Sponsored Ad: Click Here to Open a Share Trading Account Online for FREE and Pay ZERO Brokerage to Buy and Sell Shares!!!

One of the best things about this website is that I come to know some amazing and some not so amazing traders in India.

Well unfortunately most traders are losing money. 🙁 Why people lose money is that they do not have a trading plan to execute when their prediction goes wrong. They simply do not know where to take a stop loss or to book a profit. I mean when you trade you should have a trade plan in place. You should know clearly when to take a stop loss and when to take out profits.

If you take a stop loss at 50% of your profits – even if you are right 50% of the times – you will make money. Risk management is the most important decision in trading which everyone forgets.

Some get too aggressive and lose money. (Aggressive traders lose the most). Some book profits at an early stage when more profits may have come. Some just start praying to Gods for help when losing money. I mean what can Gods do if you never had a trading plan or you over-traded? Some hope that one day before expiry Nifty will reverse trend and they will be able to book profits. And you know what – it gets worse on the expiry day.

Trying to make money on hope and praying to Gods when in trouble is a different chapter of trading altogether. Out of scope as far as this article is considered. 🙂 (BTW I have been there done that 😉 )

If these are your trade plans, how on earth you are going to make money?

When I lost 7 lakhs trading I thought I am one of the worst trader in the world. The day my losses touched 7 Lakhs I slapped myself – yes literally slapped. How can greed overcome me? How can I lose so much? I was young – I could have just kept the money in a FD and it would have grown at least 50% in 4 years. But once money goes it goes – it never comes back. You will have to work hard to make more money. This hard work has nothing to do with the lost money. That one pain is going to stay for long.

Today I consider 7 Lakhs as tuition fee to the stock markets. Today I know that 7 lakhs I lost was nothing compared to what some big traders lose. At least I stopped there, learned a lot from my mistakes and started learning options trading.

But traders out there just do not want to learn. If they earn a rupee they think they are smart and can earn more. And when they lose double that they blame on luck. This continues until losses runs into lakhs.

Read this and you will be in shock too. Some of the traders are running in losses amounting to tens of lakhs. One of them living in a small town in Andhra Pradesh is currently sitting at MTM (mark-to-margin) loss of Rs. 90,000,000.00 (90 Lakhs). Are you nuts? I mean most people on Earth cannot even earn that money in a decade and here is one guy who is just destroying his wealth. All this in span of two months. When I asked him why he did not take a stop-loss he said he hates taking stop loss. What an answer. Trading is a business and when in loss – you should take a stop loss or hedge your positions.

There is more. He told me there are many more people in that town who have lost more than that amount. If a small town in AP can have retail traders trading with more than 1 crore capital, then imagine how many traders are there in India trading with that much capital?

Another software engineer was sitting at a real loss of 45 Lakhs. He buys options. Well if you also do the same take this as a warning.

If its true that 95% of retail traders are losing money – imagine how much money is being sucked from the retail traders by the FIIs, DIIs, and smart retail traders.

I have found that losses do not accumulate in a day. If you put a frog in hot water, it will jump to save his life. But if you put it in cold water and boil it slowly – the frog will not come out and boil itself to death.

Which means losses keeps on accumulating and the trader brings in more money and keeps loosing. Only to realize one day that his looses are running into lakhs. By this time it is too late to recover.

All these things happen because we never have a risk management plan in place. Well most do not even have a financial plan in place. Risk management is a small portion of your financial plan. Below I will try to address both.

How do you make sure that Risk is properly managed and you do not lose more than you can afford while trading?

Here are some steps that you need to take immediately if you want a sound financial future:

1. Do not bring more than 25% of your savings into your trading account. First of all why do you want to bring too much money into your trading account? To make more money? Well if you cannot be profitable in a small account how can you be profitable in a bigger account? In fact traders who are losing money should not bring any more money into their trading account. You will lose even more. First prove yourself that you can make more than 2% profits per month in a small account on an average for the last 10 months. Once you have crossed that threshold – you can bring more money every month. Keep a fixed amount to add to your trading account every month for a certain period. Because if you bring in a lot of money at once and take a stop loss in a big trade – you can lose a lot of money. But a fixed amount will ensure a small loss.

2. If you trade on a leverage you should always hedge your position. Future and Options both are traded on leverage because you only trade with 10-15% of the value of the trade. If you make money that is good, but if you lose you will lose on the value of the transaction not on the margin blocked. This is even more important if you are keeping the position overnight. Lets say you have Rs. 50,000 in your account and you bought 2 lots of Nifty future risking everything you have in your trading account and next day there is a gap down of 300 points.

I bet you will square off your position in panic. This is what you will lose then 300 * 50 * 2 = Rs. 30,000.00. This is 60% of your trading money. Do you think you will have enough courage to ever trade again?

But had you done some kind of hedging – like buying OTM puts I am sure you losses would have reduced to 20% of your money. This will leave you with some courage to trade again.

In stock markets always risk what you can afford. The money that you cannot afford to lose should be kept in fixed return instruments. Let the financial analysts say that Fixed instruments are boring and all that – the fact is they themselves are doing exactly opposite to what they are saying.

They have a job right? So they will say what looks good, but may not work as suggested. Which is better – losing money trading or putting money in an FD that generates 9% return every year for doing nothing?

Long back I had written an article on investment opportunities in India. It is highly recommended that you read that.

Here is how you should divide you savings. I believe in 25-25-25-25 rule.

(This is my belief – yours may differ – but I believe dividing money in different assets class. This will ensure less volatility in our financial portfolio.)

This is what I do (and you can do too):

25% of what you save should get into fixed return instruments guaranteed by Government of India. These are bank fixed deposits, post office schemes, EPF, PPF etc.

25% of what you save should get into diversified equity mutual funds. Select 3-4 different mutual funds based on their last 5 years performance. Invest only in 4 or 5 star rated funds by value research. These funds should be from different fund houses and their investing style should also be different. For example you can select one large cap fund, one mid cap fund, one small cap fund, and one thematic fund in a sector you believe in. Invest through SIP (Systematic Investment Plan to take advantage of averaging your cost of buying these funds). If possible invest in Direct plans to save money. Review every year to change any fund that is not performing.

I was surprised to know that most option traders do not invest in mutual funds. Why? They do not need your time and hard work. A very qualified fund manager works on your behalf. The fee they charge is also less – so why not make use of this great opportunity? Over a long period of time good mutual funds can generate 12-15% returns a year. Without any work I think it is a fantastic return.

25% of what you save should get into good large and mid-cap equities. Yes direct buying of stocks for long term. Here too buy systematically every week or month. Never buy any stock in bulk. If you have any stock that you want to sell, its better to start a covered call rather than direct selling. That way you will still make money if the stock does not reach your call strike price.

25% of what you save every month may come into your trading account. Since this is the most riskiest of all the above investments – you should have a limit to how much big your trading account should be. This will differ from person to person but you should know your limit here. Once that limit is reached – you know that it is the maximum you will lose if anything horrible happens. Once this limit is reached – do not bring any new money to your trading account. Just reinvest the profits and compound it. Compounding is magical and therefore you need not bring more money to it once the limit is reached.

One more thing – instead of putting surplus money in your bank you can put them in a liquid mutual fund. These funds generate 8-9% returns a year. This is much more than 3.5% Indian banks give as interest. Liquid funds have no entry or exit cost – so they are as good as any bank deposit. What’s more you can invest online and withdraw money to your bank account online.

Also if you are the head of the family and your family depends on you financially, you should always buy a term insurance policy. In case something happens to you – your family will get the sum assured and at least financially they will not be worried. Buying them online will be cheaper.

Of course now days everyone has a medical/health insurance. If you don’t have one – buy as soon as possible. Don’t forget to have a family floater plan that will cover all your family members. One major health issue to any family member can make a huge dent into your savings. Health insurance is a must.

As you can see I have not included real estate, gold and ULIPs in my investments. These are one of the most sought after investments in India. But I do not like them for the following reasons:

Real Estate: Will eat up a significant portion of your savings. If you have not timed your buy correctly or were not able to negotiate well, you will find it hard to find a buyer to sell in profits. Its a big investment – it carries a major portion of your savings so you will always be worried. (I hate worrying about money) Every month you will have to pay the mortgage, pay electricity bills, municipal taxes, clean the house etc. Repairs costs money too. Mortgage costs money. If you want to rent then finding a good family for renting is not an easy job. When they leave you will have to spend a lot on repairs, paintings etc.

People like us can invest in at most two houses. One where we live and another for investments. Investment in just one real estate is a hit or a miss thing. Either you make good money when you sell or you make average or even a loss. To make good profits you have to keep it for ten years at least. And if you make only 10% compounded annually minus your expenses, you made less than what a good mutual fund could have made without any work on your part. Not a smart choice in my view. If you want to invest in real estate just buy one property where you can live.

Here are more links about why real estate is a bad investment:

http://www.iwillteachyoutoberich.com/blog/surprising-real-estate-investing-myths/

http://www.cbsnews.com/news/history-says-home-real-estate-is-a-bad-investment/

Gold: This is another investment I hate. Gold will never beat equity returns over a 10 year time frame. Still if you want to invest in Gold – you should invest in Gold ETF every month or do a SIP in a good Gold fund. Redeem them when your kids get married to buy gold and/or when you want to buy gold for any occasion.

ULIPs – Unit Linked Insurance Plans: Worst investment ever. Government of India should ban ULIPs. Even if markets give a return of 30% – ULIPs will only generate 10-15% or even a loss. Because its a costly investment. A major portion goes into buying insurance for the owner. Yes you may not get anything in return in a term insurance if you survive the term – but if something happens to you then ULIPs will not give your family the kind of money they need. It won’t solve any purpose. Moreover its market dependent. When it is redeemed and markets are down you may lose money. Keep your insurance and your investments separate and you should get better returns. ULIPs do not solve the purpose of either insurance or investments – so they should be avoided.

IMP: Every quarter you should count your worth. This will help you know your wealth and what you can expect from future. It will also tell you any mistakes you made in the past. This will help you to plan well. If you are strict with your finances, I assure you will only get richer with time.

Happy Investing and Wishing You the Best For Your Future!

Disclaimer: The views expressed in this article are of the author. Please do your own research before investing money in anything. This is the way I manage my finances and am comfortable. Your situation may be different. Therefore you may want to take a different approach. The only benefit of the above investment approach is that the finance portfolio is less volatile. However it is recommended that you do your own research before taking an investing decision. Do not take investment decision in a hurry.

Click to Share this website with your friends on WhatsApp

COPYRIGHT INFRINGEMENT: Any act of copying, reproducing or distributing any content in the site or newsletters, whether wholly or in part, for any purpose without my permission is strictly prohibited and shall be deemed to be copyright infringement.

INCOME DISCLAIMER: Any references in this site of income made by the traders are given to me by them either through Email or WhatsApp as a Thank You message. However, every trade depends on the trader and his level of risk-taking capability, knowledge and experience. Moreover, stock market investments and trading are subject to market risks. Therefore there is no guarantee that everyone will achieve the same or similar results. My aim is to make you a better & disciplined trader with the stock trading and investing education and strategies you get from this website.

DISCLAIMER: I am NOT an Investment Adviser (IA). I do not give tips or advisory services by SMS, Email, WhatsApp or any other forms of social media. I strictly adhere to the laws of my country. I only offer education for free on finance, risk management & investments in stock markets through the articles on this website. You must consult an authorized Investment Adviser (IA) or do thorough research before investing in any stock or derivative using any strategy given on this website. I am not responsible for any investment decision you take after reading an article on this website. Click here to read the disclaimer in full.

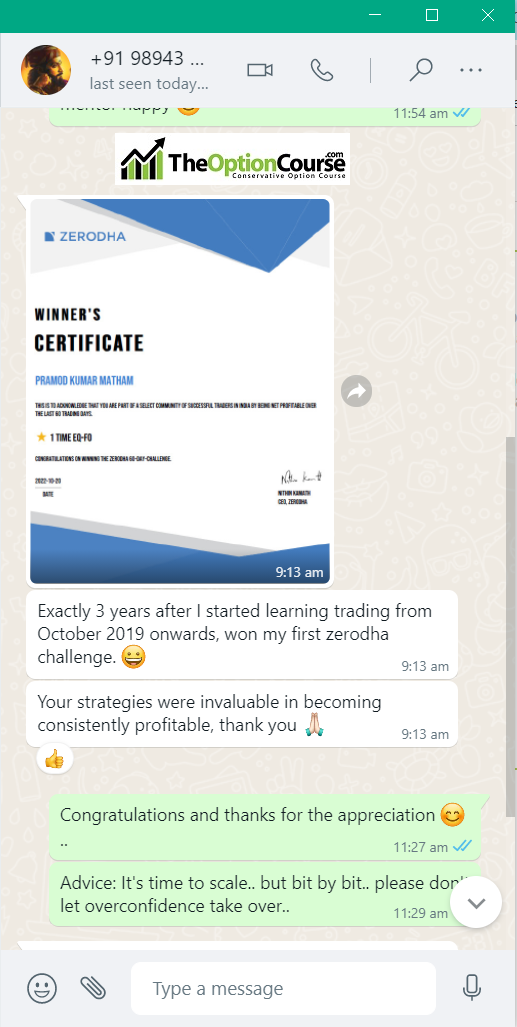

My student gets the Winner's Certificate of Zerodha 60-day Challenge - Click here and Open Stock Buy and Sell Free Account with Them Today!!!

Testimonial by a Technical Analyst an Expert Trader - Results may vary for users

Testimonial by a Technical Analyst an Expert Trader - Results may vary for users

60% Profit Using Just Strategy 1 In A Financial Year – Results may vary for users

60% Profit Using Just Strategy 1 In A Financial Year – Results may vary for users

Testimonial by Housewife Trader - Results may vary for users

Testimonial by Housewife Trader - Results may vary for users

Comments on this entry are closed.

I get a feeling that You seem to be genius in many ways.

However I beg to differ with your views on real estate investment because of the reason,India can’t be compared to US on this issue because of population versus land ratio .

I mean that density of population ratio in India is atleast 10 times higher than US (After discounting other factors like US has more richer , affordable population)

I personally know many people who bought/inherited land for peanut value , who atleast on paper are multi-millionaires.

Jacob, I am not a genius in any way – I work hard 🙂

1. Most of the people whom you know DID NOT invest in real-estate to make money – they got lucky in the sense they bought land/flat for whatever reasons at that time WITHOUT knowing that its value will quadruple in a few years time. Hint: Farmers becoming crorepatis in Gurgaon.

2. Real estate needs substantial investments. You first need to buy a house for your family to live. This is not investment – this is need. Only after that you can buy a property for investment purposes. Only the best locations give great value in future. For most people in India (average middle class) this is unaffordable.

3. Even after the investment with a loan – the cost of paying back the loan, registration and maintenance will make a huge dent in the returns. Only a few people can make a decent return on real estate. Decent return means more that 20% compounded per year after all expenses are deducted. This is very difficult even for people in this business. They make money because they flip the project for cash after its finished for profit. It is their business not investment.

4. God forbid if someone is unable to pay back the home loan on an invested project. Foreclosure will kill the living joy out of that person. Facing foreclosure not only dejects a person but also has other very bad financial implications. He may never ever get a loan – I mean ANY loan. No body wants to be in that situation. Unfortunately in India he will earn a bad reputation in the society too.

5. And finally even if it gives a return of 10% compounded annually after all other costs – that person still lost money because a good equity fund will deliver better returns over 5-6 years. Compare this to all the hassles one needs to go through in a real estate investment. On the other hand you just need to fill a form and give a check to invest in mutual funds.

6. Tax efficiency: Profits are taxed in Real Estate even if you sell it after 10 years. After 1 year returns from equity mutual funds are tax free. 🙂 After taxes effectively returns will be very poor in real estate.

7. Try to find people who invested in real estate (taking a risk at that time) to make money. Exclude the ones who got lucky. You will rarely find those people. 🙂

Thanks for the question.

Dear Sir,

I am reading all your articles regularly. Your writings are 1000% applicable to reality traders. I have also lost huge money in stock market. But, I learnt so many things and I also treated the loss as huge fees for learning lesson from my mistakes in trading.

I made research and learnt chart reading and analysing technical indicators. One has to learn from his mistakes. No body is greater than Market. We have to follow the trend of the Market. We cannot ride or dictate the Market.

Being a small fish in the ocean ( being small retails trader), we have to learn to live in the Market (ocean) before big fishes like shark, wale, etc., ( like FIIs, DIIs, etc.,) .

All your articles are heart touching and one must learn from these articles.

Thanks & Regards,

Ravindra

Bangalore

Ravindra,

Thanks for the kind words. 🙂

Why do you think retail traders are small fish in the big ocean? Why do you take yourself to be so weak that you have already surrendered to the institutional investors even before the fight has began. Is anybody forcing you to trade? If you think you will only make losses, then please either change the mindset or stop trading else you will only make losses.

You said that you are learning technical analysis. I am sure after learning your results must have improved. But if they haven’t and if you are still losing money, there is no one forcing you to trade except you.

My only advice is. Do not think yourself to be weak. If you trade thinking your money will be taken by institutional investors, they will actually take your money away.

Be positive, get some correct knowledge and trade.

Please hedge your positions and never trade Intraday. You will see that your results have improved.

Best.